All Categories

Featured

Table of Contents

- – What resources do I need to succeed with Infin...

- – Is Infinite Banking Account Setup a good strat...

- – Infinite Banking For Retirement

- – What is the minimum commitment for Infinite W...

- – Bank On Yourself

- – How secure is my money with Policy Loans?

- – Can I use Infinite Banking to fund large pur...

The concept behind limitless banking is to use this money worth as a source of funding for different purposes, such as investments or individual costs, while still gaining compound interest on the money value. The idea of unlimited banking was first proposed and popularised by Nelson Nash, a financial consultant and author of guide "Becoming Your Own Banker".

The insurance holder obtains versus the money value of the plan, and the insurer bills passion on the financing. The rate of interest rate is typically lower than what a bank would charge. The insurance policy holder can utilize the loaned funds for various purposes, such as spending in actual estate or beginning a business.

Nonetheless, it is crucial to keep in mind that the insurance holder must not just pay the home mortgage on the financial investment home however likewise the passion on the policy loan. Policy loan strategy. The interest payments are made to the insurance policy agent, not to oneself, although the insurance holder might receive returns as a shared insurance provider's investor

This stability can be attracting those that choose a traditional strategy to their financial investments. Unlimited financial offers policyholders with a source of liquidity via plan financings. This suggests that even if you have borrowed versus the money value of your plan, the money value proceeds to grow, using flexibility and access to funds when required.

What resources do I need to succeed with Infinite Banking?

The survivor benefit can be used to cover funeral expenses, arrearages, and various other expenses that the family may sustain. In enhancement, the survivor benefit can be invested to offer long-term monetary security for the policyholder's household. While there are possible advantages to infinite banking, it's vital to consider the downsides too: One of the key objections of boundless banking is the high costs connected with whole-life insurance plan.

Additionally, the fees and compensations can eat into the money worth, minimizing the general returns. When utilizing infinite financial, the insurance holder's financial investment alternatives are limited to the funds available within the plan. While this can offer security, it might also restrict the capacity for higher returns that might be accomplished with other investment cars.

Is Infinite Banking Account Setup a good strategy for generational wealth?

Take into consideration the case where you acquired one such policy and carried out a thorough analysis of its performance. Then, after 15 years right into the policy, you would certainly have found that your plan would have deserved $42,000. Nevertheless, if you had just saved and spent that money instead, you might have had even more than $200,000.

To completely assess the stability of boundless financial, it's important to recognize the fees and fees associated with entire life insurance policy plans. These costs can differ depending on the insurance provider and the details policy. Privatized banking system. Premium cost charge: This is a percent of the costs quantity that is deducted as a cost

Infinite Banking For Retirement

Each fee: This cost is based upon the death advantage quantity and can vary depending upon the plan. Cost of insurance coverage: This is the expense of the needed life insurance policy protection related to the plan. When calculating the possible returns of a boundless banking strategy, it's important to consider these costs and fees to identify truth worth of the cash value growth.

These individuals usually mean to market the concept and minimize fee effects. To avoid making blunders and losing cash, it is recommended to maintain your monetary approach simple. If you need life insurance policy, opt for term insurance coverage, which supplies coverage for a particular period at a reduced expense. By doing so, you can assign the conserved costs in the direction of investments that offer higher returns and greater versatility.

What is the minimum commitment for Infinite Wealth Strategy?

Pension: Adding to pension such as Individual retirement accounts or 401(k)s can offer tax benefits and long-term development possibilities. It is necessary to check out different options and seek advice from an economic consultant to figure out which approach aligns ideal with your financial objectives and run the risk of resistance. Currently that you have a thorough understanding of limitless financial, it's time to review whether it's the ideal approach for you.

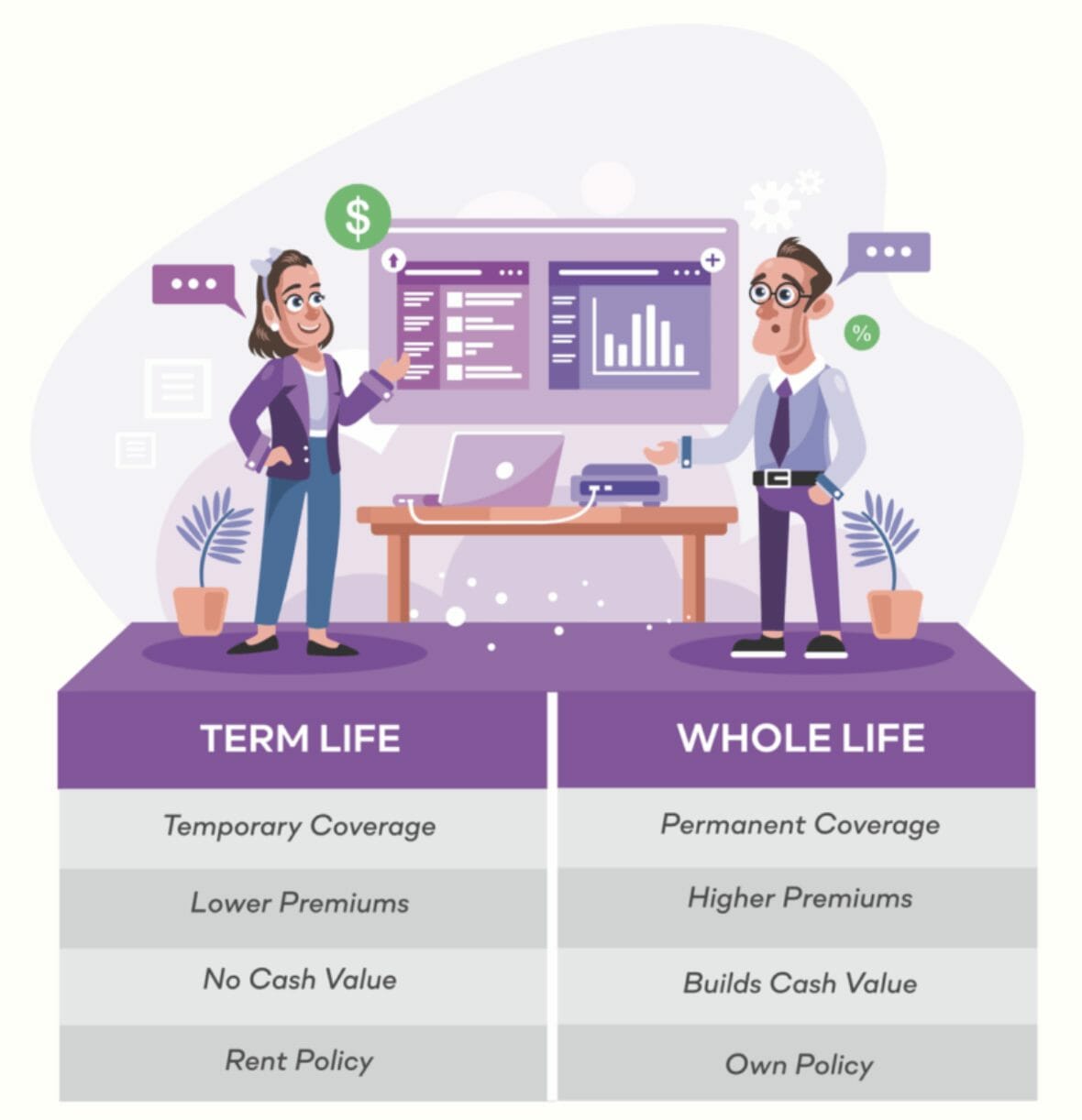

At the very same time, term life insurance policy does not offer any kind of cash value, indicating that you will certainly not get anything if you outlast the policy. In addition, term life insurance policy is not long-term, implying that it will expire after a specific time period. Unlimited financial can be a great idea for individuals who are seeking a lasting financial investment strategy and that are prepared to make considerable capital expense.

Bank On Yourself

This site supplies life insurance policy details and quotes. Each rate shown is a quote based on information supplied by the service provider. No part of may be duplicated, published or distributed in any manner for any kind of objective without prior composed permission of the proprietor.

Think of this for a minute if you could somehow recoup all the passion you are presently paying (or will pay) to a financing organization, just how would certainly that boost your wealth producing potential? That includes charge card, auto loan, student car loans, service loans, and also home mortgages. The average American pays out $0.34 of every gained buck as a passion expense.

How secure is my money with Policy Loans?

Picture having actually that passion come back to in a tax-favorable account control - Infinite Banking vs traditional banking. What possibilities could you make use of in your life with also half of that cash money back? The keynote behind the Infinite Financial Principle, or IBC, is for people to take even more control over the funding and banking functions in their daily lives

IBC is a strategy where individuals can essentially do both. By having your dollar do more than one work. Possibly it pays a bill.

Can I use Infinite Banking to fund large purchases?

It can do absolutely nothing else for you. Yet what if there was a method that instructs individuals how they can have their $1 do than one work just by relocate with a possession that they control? And what if this strategy came to the day-to-day individual? This is the essence of the Infinite Banking Principle, initially championed by Nelson Nash in his publication Becoming Your Own Banker (Wealth management with Infinite Banking).

In his publication he demonstrates that by developing your very own private "banking system" with a particularly developed life insurance policy contract, and running your bucks with this system, you can substantially improve your financial scenario. At its core, the concept is as easy as that. Creating your IBC system can be done in a selection of creative ways without transforming your capital.

{kind=link}

Table of Contents

- – What resources do I need to succeed with Infin...

- – Is Infinite Banking Account Setup a good strat...

- – Infinite Banking For Retirement

- – What is the minimum commitment for Infinite W...

- – Bank On Yourself

- – How secure is my money with Policy Loans?

- – Can I use Infinite Banking to fund large pur...

Latest Posts

Infinite Banking Concepts

How To Set Up Infinite Banking

Cash Flow Banking With Life Insurance

More

Latest Posts

Infinite Banking Concepts

How To Set Up Infinite Banking

Cash Flow Banking With Life Insurance